Keep knowledgeable with free updates

Merely signal as much as the International Financial system myFT Digest — delivered on to your inbox.

The “Japanification” of China continues to be a giant theme, with a lot of eerie parallels right right down to stimulus proving wanting. Right here’s the most recent symptom:

Yep, the 30-year authorities bond yields of China and Japan are on the cusp of crossing paths for the primary time (ever, we predict, however LSEG information for each 30-year benchmarks doesn’t go additional again than 2009).

At pixel time there’s nonetheless a 8.7 foundation level unfold between the 2 long-term bond yields, with the Chinese language 30-year yielding 2.245 and the Japanese 30s buying and selling at 2.158 per cent. But it surely seems to be like that gained’t final lengthy. Shorting Chinese language authorities bonds actually has been the new widow-maker trade.

The fading yield curve differential is one other stark manifestation of China’s rising financial and demographic malaise, and Japan’s (for now) success in lastly profitable a three-decade battle in opposition to deflation. As Barclays economists mentioned in a giant report on whether or not China can escape the same destiny:

China’s accelerated financial improvement was paying homage to Japan’s postwar financial miracle. Furthermore, China was in sure quarters as soon as anticipated to overhaul the US because the world’s largest economic system by 2035.

Nonetheless, after many years of quickly narrowing the hole to the US, since 2022 China has began dropping floor. Surpassing the US economic system now seems a distant hope; its weakening labour market, declining agency profitability, slumping housing exercise, and adversarial debt-deflation dynamics have raised issues about China’s longer-term progress outlook.

. . . We predict China’s deleveraging journey has solely simply began, and it’s unlikely to be accomplished earlier than 2030, which means the structural headwinds to consumption and funding will persist.

It ought to be famous that there’s nonetheless a decent-sized if narrowing hole between China and Japan on the 10-year a part of the curve. However on the even longer finish of the curve, yields have already crossed, with the Japanese authorities bond maturing in March 2064 at the moment yielding 2.472 per cent, and China’s November 2064 bond buying and selling at 2.275 per cent.

The parallels between Japan within the early Nineties and China immediately are myriad, Barclays famous in its report. FT Alphaville’s emphasis under:

The financial circumstances going through China have parallels with Japan’s expertise after its asset bubble burst within the early Nineties. This created the time period ‘Japanification’, which is often outlined as a mix of gradual progress, low inflation, and a low coverage charge, accompanied by deteriorating demographic tendencies.

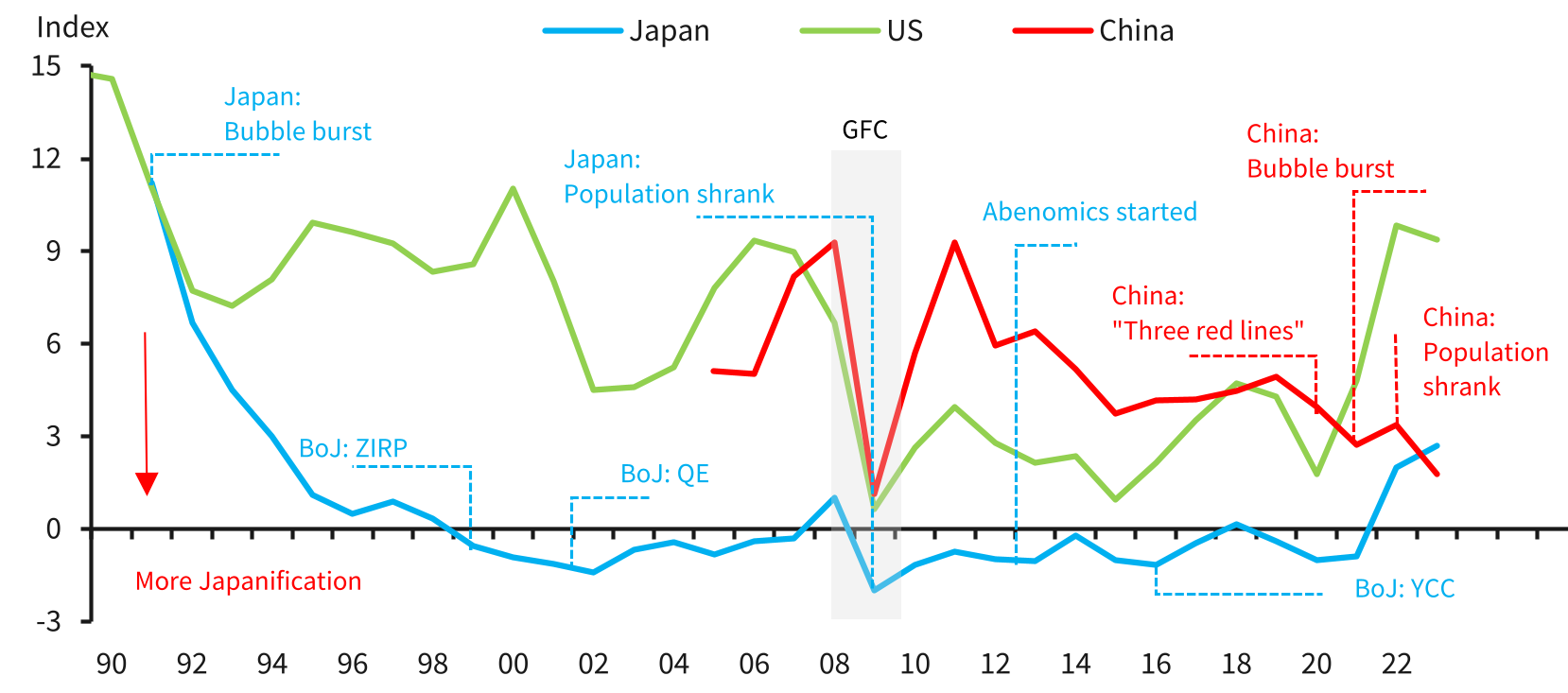

To measure this phenomena, a Japanese economist, Takatoshi Ito, launched a Japanification Index, which measured the sum of the inflation charge, nominal coverage charge, and GDP hole. To use to China’s economic system, we have now adjusted this index, changing the GDP hole with working-age inhabitants progress, because the estimation strategies of GDP gaps differ throughout nations and working-age inhabitants is by far probably the most basic determinant for long-term progress. Our amended index exhibits that China’s economic system has turn into extra ‘Japanised’ than Japan’s just lately, albeit marginally.

This not a shock to us. A demographic drag, the emergence and collapse of asset bubbles, debt overhang, zombie firms, deflationary pressures from extra capability/excessive debt, and excessive youth unemployment, to call just a few, are a few of the notable similarities between the economies of China and Japan submit their bubbles.

And right here’s that index.

{kind=link}